10 financial challenges many women over 40 may face

An expert shares some of the ways women over 40 can empower themselves financially.

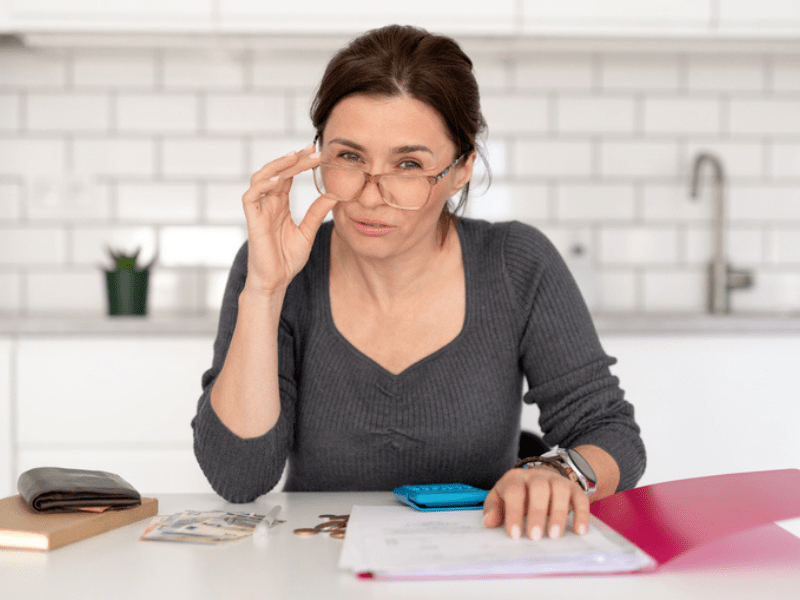

Women over 40 are often expected to have their finances in order.

However, many are juggling complex financial responsibilities, sometimes for the first time in their lives.

This midlife stage, which should ideally bring greater confidence and stability, can instead be marked by sudden life shifts and insecurity.

South Africa's Women’s Month 2025 theme is 'Building Resilient Economies For All'. It's a timely reminder of the need to create inclusive financial systems that support all women.

“This is an ideal opportunity to highlight the financial challenges many women face in midlife, and to encourage open, empowering conversations about money,” says Sarah Nicholson, platform and customer experience manager at JustMoney.co.za, a personal finance platform that helps South Africans make good choices.

“Much advice is geared towards younger women and career growth, but it is equally important to support those in midlife who are navigating pivotal life transitions.

“By recognising their realities and sharing practical strategies, we can help more women build resilience and regain financial confidence when so much in their lives is changing.”

ALSO READ: Three tips from a CA to level up your finances

Nicholson lists 10 challenges many women may face at midlife.

- Divorce or separation. Many women face a sudden loss or reduction of household income, legal fees, and the challenge of rebuilding finances on a single income.

- Job loss or career interruption. Midlife women may experience retrenchment, age discrimination in the job market, or voluntary/involuntary career breaks.

- Caring for ageing parents. The responsibility of looking after elderly parents, both emotionally and financially, can fall heavily on women, often without support.

- Supporting adult children. Many women continue to assist adult children financially, whether helping with education, rent, or childcare, delaying their own savings goals.

- Limited retirement savings. Women often have lower lifetime earnings due to wage inequality, career breaks, or part-time work, resulting in smaller retirement funds.

- Longer life expectancy. Women tend to live longer than men, which increases the need for more substantial retirement savings to maintain quality of life.

- Lack of financial literacy. Some midlife women may not have been involved in long-term financial decision-making, especially if a partner handled finances, making it harder to navigate these later in life.

- Health issues and rising medical costs. Increased health risks come with age, and women may face higher out-of-pocket costs, especially if they don’t have comprehensive medical cover.

- Widowhood or loss of a partner. The death of a spouse or long-term partner can bring financial instability, especially if they were the main breadwinner or had sole control of finances.

- Estate and inheritance issues. Poor estate planning or lack of access to shared assets can leave women financially vulnerable if a partner dies, or there is a family dispute.

“It is so important to talk about money. Don’t keep financial stress to yourself. Money conversations break the silence and open doors to solutions," advises Nicholson.

Women over 40 can reset and rebuild their finances with the right mindset and advice. JustMoney shares the following tips.

- Empower yourself with knowledge. If you’ve left financial decisions to someone else, now is the time to inform yourself. Speak to a certified financial adviser and read finance-related books, articles, and newsletters to build your knowledge and confidence.

- Get legal advice if considering divorce. Decisions you make now have long-term financial, emotional, and legal consequences. A family lawyer can help ensure you understand your rights regarding property, pensions, maintenance, and child custody, so you don’t unknowingly agree to an unfair settlement.

- Get smart about budgeting. Track your income and expenses closely. Identify areas where you can cut back, and redirect these savings to debt repayments, investments, or essential needs like medical cover.

- Build (or rebuild) an emergency fund. If you’ve been through divorce, retrenchment, or other disruptions, aim to save at least three to six months’ worth of living expenses to create a financial cushion.

- Boost your retirement savings. Increase your retirement fund payments if possible. A financial adviser can help you assess how much you’ll need and whether you're on track.

- Protect your income. Consider income protection or disability cover, especially if you’re self-employed or single. Your ability to earn is your greatest asset.

- Review your medical aid and insurance. Ensure your health cover and short-term insurance suit your current needs. Avoid overpaying for outdated policies.

- Plan for caregiving responsibilities. Be honest about what you can afford, explore shared costs with other family members, and check if elderly parents meet the means tests for social support options. Some municipalities offer discounts on rates and services, such as electricity and water, for qualifying senior citizens. The monthly South African Social Security Agency (SASSA) grant is R2,315 per month for those aged 60-74 years, and R2,335 per month for those aged 75 years and over.

- Prioritise debt reduction. Pay down high-interest debt, such as credit cards or loans. Avoid taking on new debt to support family unless it’s manageable and planned for.

- Update your will. Make sure your legal affairs are up to date, including your will, beneficiaries, and any power of attorney arrangements. This protects your assets and your loved ones.

- Consider a side hustle or second career. Many women use this stage of life to pivot, monetise skills, or explore passion projects, providing both income and a sense of purpose.

Nicholson says life changes, and your financial plans should be in alignment.

“Whether you’re navigating a divorce or career change, or caring for loved ones, your financial strategy needs to reflect where you are now, not where you were five or 10 years ago. Staying flexible and proactive is the key to building long-term financial security.”

Where to turn for support

- The Financial Planning Institute of Southern Africa (FPI) is a professional body for certified financial planners and other qualified professionals. Search the website to find a financial planner. Email [email protected] to verify a planner.

- Find a lawyer in your area at https://www.attorneys.co.za. Email [email protected] or call 0861 114 619.

- Legal Aid South Africa, a government-funded organisation, provides free legal services to those who cannot afford private lawyers. Go to https://legal-aid.co.za/ or call 0800 110 110.

- The South African Depression and Anxiety Group (SADAG) provides free help for people struggling with mental health issues, such as depression, anxiety, and trauma. Go to https://www.sadag.org/, SMS 31393 or call 0800 567 567.

- The Businesswomen's Association of South Africa (BWASA) is a non-profit organisation dedicated to empowering and supporting women in business. Go to https://bwasa.co.za/.

Listen to Jacaranda FM:

- 94.2

- Jacaranda FM App

- http://jacarandafm.com

- DStv 858/ OpenView 602

Follow us on social media:

MORE FROM JACARANDA FM:

Main image credit: iStock