Money lessons parents need to teach their children

From allowance budget tips to ‘parent-backed loans’, here's how to teach your children about money from as early as three-years-old.

Children don't have to worry about paying bills such as rent, food or car loans, but that doesn't mean they shouldn't learn about money.

Recent studies show that 12 million South African adults are over-indebted, with many relying on their credit cards to buy basics such as food.

Other reports reveal that SA's financial literacy is just 51%. Financial education is strongly linked to economic empowerment, which is why good money habits should start early.

The lessons that children learn from their parents about saving, spending, and making choices with money often stay with them for life.

That’s why it’s important to begin teaching financial basics as soon as possible. But which lessons matter most, and when should we teach them?

Behavioural researchers from the University of Cambridge recommend starting money lessons as early as age three. At this age, children begin forming money habits through saving and simple decision-making play.

By age seven, most children can grasp the value of money, understand delayed gratification, and realise that some choices are irreversible and may affect them in the future.

South African studies bear out parents’ influence in shaping their children’s attitudes towards money.

A 2023 UNISA survey in rural and low-income communities found that parental financial communication is significantly positive for financial decision-making in young adults.

A Nelson Mandela University study in 2019 found that talking about money, modelling behaviour and involving children in small financial tasks were linked to more responsible financial behaviour.

Gavyn Letley, a father and Product Head at DirectAxis, says the earlier children start learning about money, the better.

“All the international and local evidence points to early parental involvement, experiential learning, and real-world scenarios consistently resulting in better outcomes when dealing with money during adolescence and adulthood.”

Of course, making the money lessons age-appropriate is important, and Letley suggests the following guidelines.

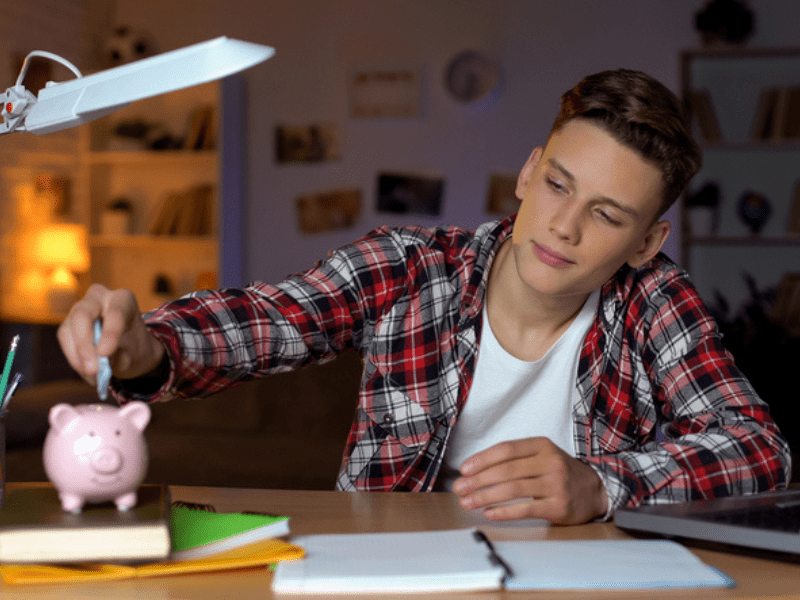

Age 3 – 5: Learning delayed gratification

The Rolling Stones were right, in 1969, when they sang, “you can’t always get what you want”. Fifty-six years later, this still rings true. In an era of instant gratification, from takeaway foods to online shopping, teaching children early that some things are worth waiting for will encourage them to save for what they want. Learning this lesson early means that later in life, they’ll be less tempted to use credit to get what they want instantly.

Use a savings jar or piggy bank to keep birthday money or small rewards for chores, good behaviour, or achievements. Set them up for success by setting achievable goals, so they don’t lose sight of what they’re saving for.

Each time money is added to their savings, let the child count it and help them work out how much more is needed to reach their target.

“Letting younger children handle cash under supervision is a good idea. Physically counting money manifests how their savings are growing and makes them think a little harder about how they spend it.”

Age 6 – 10: Financial responsibility and simple budgets

Use pocket money or earnings from doing household chores to explain financial priorities. Help them allocate money for expenses, such as contributing to a pet’s upkeep. Set aside some savings for longer-term goals, such as buying a Lego set or a skateboard. Also, make an allowance for treats, so learning to manage money gives them some enjoyment.

Practical experience is the best way to drive money lessons home. Take them grocery shopping to reinforce that you need to buy the essentials before buying any luxuries.

“The point is to give children a realistic understanding of how to manage money, using familiar examples. They’re far more likely to grasp this than abstract explanations,” says Letley.

Age 11 – 13: Long-term goals and interest

Introduce bigger goals and explain opportunity cost – trading short-term gratification for larger rewards.

Often in the pre-teen or early-teen years, children are reluctant to save because they’re more focused on short-term goals, such as buying snacks at school, clothes or more mobile data. By setting longer-term financial targets that will allow them to get items they really want, they’ll learn how sacrificing some short-term non-essentials enables them to get that PlayStation sooner.

You can also start teaching them about compound interest – how, by saving over a longer period, they benefit from the compounding effect because they earn interest on the money that they’ve saved as well as the accumulated interest.

When saving larger amounts of money, it’s sensible and safer to replace the piggy bank or savings jar with a bank account. Some banks offer a transactional account with no fees for under-18s, such as the FNBy account. Doing this will also teach them how to manage a bank account.

READ: Money saving tips during tough financial times

Ages 14 – 18: Borrowing wisely and credit awareness

As children grow up, their earning potential increases. They may graduate from household chores to a casual job. Typically, their expenses also increase at this point. They may want a new bicycle, a scooter, a motorbike, or to start saving towards a car.

At some point, they’ll probably ask to borrow money. When they do, structure ‘parent-backed loans’ with timelines, interest, and a repayment schedule to simulate real-world borrowing.

Explain that there will be penalties for missing payments and that if they do, you’ll be less likely to lend them money in future. They’ll probably think you’re being harsh, but it will teach them valuable lessons about the benefits of paying what they owe on time and building a good credit record.

“As a parent, teaching children about money isn’t something you’ll ever stop doing. Perhaps the most important lesson is to remember that you’re a role model. It’s not just what you teach them, but your financial behaviour that will influence their relationship with money and how well they manage their finances as adults,” says Letley.

Listen to Jacaranda FM:

- 94.2

- Jacaranda FM App

- http://jacarandafm.com

- DStv 858/ OpenView 602

Follow us on social media:

MORE FROM JACARANDA FM:

Main image credit: iStock